Introduction

Protecting customer information has never been more critical. The Payment Card Industry Data Security Standard (PCI-DSS) stands as a cornerstone in safeguarding payment card data. However, for many business owners, technology managers/directors, and business executives, navigating the complexities of PCI-DSS can be daunting. This guide aims to demystify PCI-DSS, and break down its key components into understandable segments, ensuring you’re well-equipped to secure your business and comply with this essential standard.

What is PCI-DSS?

The Payment Card Industry Data Security Standard (PCI-DSS) represents a universally recognized framework of security measures aimed at safeguarding card transactions and data. Initiated and maintained by the PCI Security Standards Council, composed of leading credit card organizations, PCI-DSS sets the benchmark for all entities that interact with credit card information. This includes a broad spectrum of activities involving cardholder data.

Who Needs to Comply with PCI DSS?

The reach of the Payment Card Industry Data Security Standard (PCI-DSS) extends far beyond just merchants and service providers. It casts a wide net, encapsulating all entities involved in the handling of cardholder data. This includes organizations that store, process, and/or transmit cardholder data, as well as any technical and operational system components included in or connected to this data. The following sections clarify who needs to comply:

- Merchants

- Whether an organization is a cozy cafe in a bustling city or an online store reaching customers worldwide, if such accepts card payments, PCI-DSS applies to it. In fact, it applies to any business regardless of size or transaction volume, that accepts or processes payment cards. This is not limited to physical retail stores, online merchants, B2B companies, and any other entity directly dealing with payment cards are included.

- Service Providers

- Organizations that play a role in processing, storing, or transmitting cardholder data for others, are defined as service providers under PCI-DSS. This includes companies offering payment processors, hosting services, outsourced IT services and even data processing solutions. If a service has any interaction with payment transactions or cardholder data, compliance with PCI-DSS is mandatory.

- Financial Institutions

- Banks, credit unions, and payment card issuers are also under the umbrella of PCI-DSS, given their roles in processing and managing payment card transactions. As key players in the payment card data ecosystem, these financial institutions are subject to multiple regulatory standards that mirrors aspects of PCI-DSS. This includes compliance with regulations like the Gramm-Leach-Bliley Act (GLBA), the General Data Protection Regulation (GDPR), the Sarbanes-Oxley Act (SOX) and the Federal Financial Institutions Examination Council (FFIEC).

- Payment Gateways and Processors

- Companies that facilitate the processing of payment card transactions, act as the intermediaries between merchants and financial institutions.

- Other Entities

- Any organization that plays a role in the payment card processing ecosystem, including those that may indirectly impact the security of cardholder data, must adhere to PCI-DSS. This broad category ensures a comprehensive approach to securing cardholder data across the entire transaction process.

The Benefits of PCI DSS Compliance

At its heart, PCI-DSS compliance is about understanding cyber threats and proactively reducing the risk they pose to business functions. This consequently builds trust and resiliency among customers, partners and stakeholders. Most importantly, since digital transactions are the norm, ensuring adequate security of customers’ payment card data is critical. Lastly, compliance with PCI-DSS helps an organization in at least the following ways:

- Minimize the Risk of Data Breaches: Implementing the security measures outlined in PCI-DSS significantly reduces the likelihood of sensitive information falling into the wrong hands. According to Security Magazine, a cybersecurity industry magazine, there are over 2,200 cyber attacks every day – 1 attack every 39 seconds.

- Build Trust: Customers, partners and stakeholders are more likely to do business with you if they feel confident that customer data is handled with care and security. Additionally, being able to advertise compliance with PCI-DSS guidelines and beyond will likely open many more doors to partnerships and client business. Moreover, some partners exclusively work with entities that are compliant with regulations like PCI-DSS.

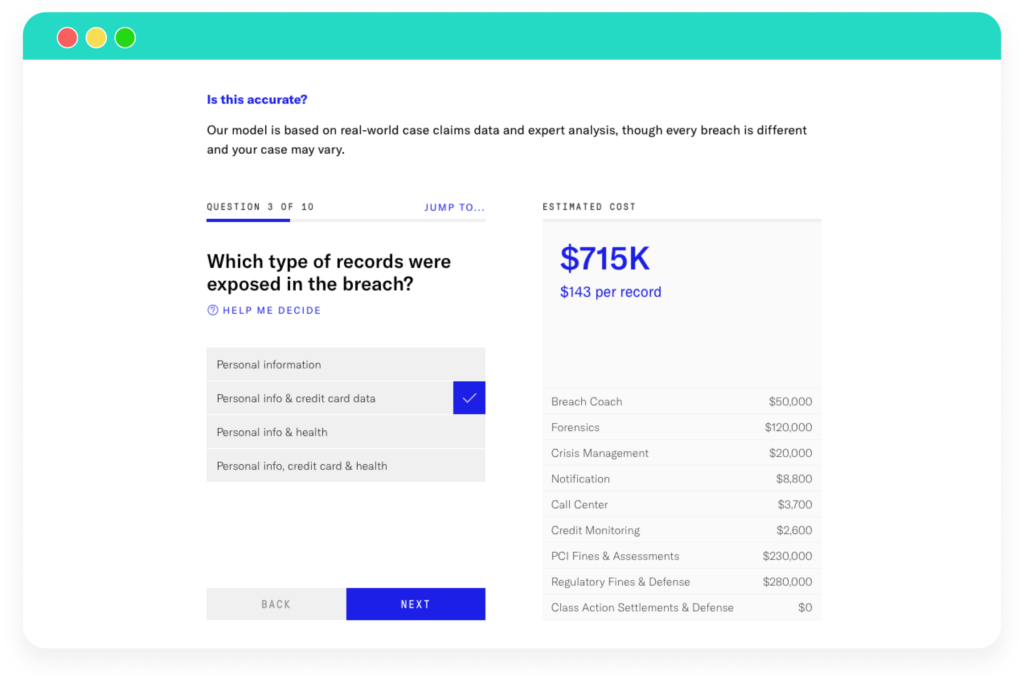

- Avoid Financial Penalties: Non-compliance can lead to hefty fines and, in some cases, losing the ability to process card payments altogether. Cyber Insurance company At-Bay, showcases a cyber risk calculator from real-world case claims data that demonstrates the possible costs resulting from a breach of payment card data. The following image depicts an illustration of a breach of 5,000 cardholders’ data from the At-Bay’s website.

Cyber risk calculators: AT-bay. At. (2023, December 19). https://www.at-bay.com/cyber-risk-calculators/

Consequences of Non-Compliance

Failing to comply with PCI-DSS can have severe consequences. Beyond the immediate financial penalties, non-compliance can damage reputation, lead to loss of customer trust and, and ultimately, future business revenue. It can also tarnish relationships to service providers, banks and other entities. Moreover, it can also put you at odds with broader regulations like the EU GDPR (General Data Protection Regulation), further compounding the financial and legal ramifications.

- Financial Penalties: Non-compliance with PCI DSS can lead to substantial fines imposed by PCI enforcement entities, ranging from $5,000 to $100,000 per month for violations. These costs trickle down to the merchants, significantly impacting their financial health. In severe cases where a breach is implicated, merchants may face additional fines compounding financial burdens. For example, in 2017, Target faced an $18.5M fine from one of the largest data breaches affecting millions of consumers.2

- Operational Risks: Beyond fines, acquiring banks may revoke a non-compliant merchant’s ability to process card payments, cutting off a vital revenue stream.

- Increased Compliance Obligations: In the event of a breach, the road to recovery is steep, with increased scrutiny and compliance obligations. This scenario often entails more rigorous audits, enhanced security measures, and, in some cases, mandatory enrollment in costly compliance programs.

- Relationships with Banks and Insurance Companies: Banks and cyber insurance companies assess the risk profile of businesses before working with them or providing coverage. Non-compliance with PCI DSS raises red flags, leading to refused partnerships or insurance claims, especially in the aftermath of a security incident. This lack of support can further isolate businesses, leaving them vulnerable to future risks.

- Global Regulatory Implications: It’s also crucial to recognize the broader legal landscape, particularly with regulations like the EU GDPR. A breach of cardholder data not only violates PCI DSS but can also infringe upon GDPR, attracting penalties up to €20 million or 4% of annual global turnover, whichever is greater. These regulations underscore the global consensus on the importance of data security and the severe repercussions for lapses in compliance.

To conclude, PCI-DSS covers a wide range of entities that interact with cardholder data. It is a standard, not a law. However, severe consequences for non-compliance can have devastating effects on an organization’s health. Meeting these standards, on the other hand, will positively impact its security, and trust. The next episode of this series will focus on how an organization becomes PCI-DSS compliant. Additionally, it will introduce the 12 PCI-DSS requirements and its six control objectives.

If you want to learn more about how our team can help you meet regular penetration testing requirements, we invite you to schedule a free consultation call. We would be happy to help you on the journey to compliance.

Schedule a free consultation

Resources

Achieving compliance is a journey, not a destination. Here are some resources to help you on your way:

- Official PCI Security Standards Council (PCI SSC) Website: https://www.pcisecuritystandards.org/document_library/

- For comprehensive guides and documentation.

Glossary: Understanding PCI-DSS Terms

To help you navigate the world of PCI-DSS with ease, here’s a glossary of terms used in this article:

- PCI-DSS (Payment Card Industry Data Security Standard): A set of security standards designed to ensure all companies that accept, process, store, or transmit credit card information maintain a secure environment.

- Cardholder Data: Any information printed, processed, transmitted, or stored in any form on a payment card. Includes the card number, cardholder’s name, expiration date, and security codes.

- Merchant: A business that accepts credit or debit card payments for goods or services.

- Service Provider: A company that processes, stores, or transmits cardholder data on behalf of another entity, or that could affect the security of the cardholder data environment.

- GDPR (General Data Protection Regulation): A regulation in EU law on data protection and privacy in the European Union and the European Economic Area. It also addresses the transfer of personal data outside the EU and EEA areas.

- Disclaimer: The Image shows a fictitious estimate. Every breach is different and may require additional remediation costs and requirements based on industry, regulations, federal, state and local laws. Image intended for educational purposes only. ↩︎

- Target to pay $18.5M for 2013 data breach that affected 41 million consumers: USA Today. (2017, May 23). Retrieved from https://www.usatoday.com/story/money/2017/05/23/target-pay-185m-2013-data-breach-affected-consumers/102063932/ ↩︎